Budget summary 2016

Personal tax

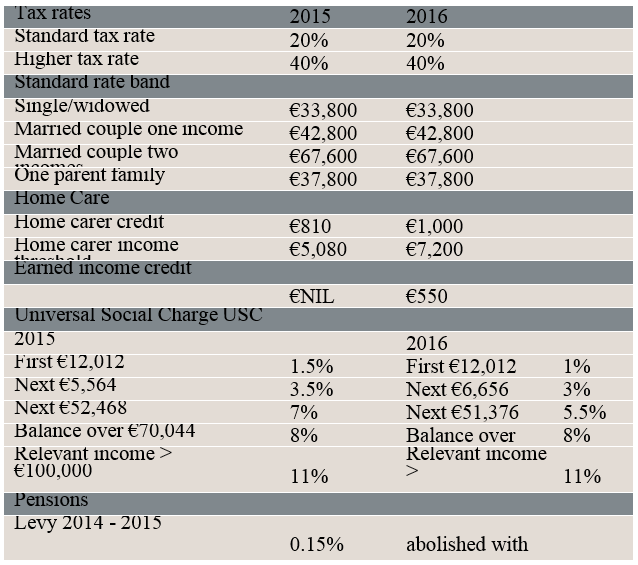

Tax rates and bands

No changes to income tax rates or bands.

USC bands and rates

Favorable adjustments to the lower USC bands and rates. Rates reduced to 1%, 3% and 5.5% with some adjustments to the bands. The rate of 8% for income over €70,044 and the 11% rate for relevant income over €100,000 remain unchanged.

Entry threshold for USC increased from €12,012 to €13,000 i.e. where income is less than €13,000 it is exempt from USC.

PRSI

A tapered PRSI credit (maximum level of €12 per week) for employees insured at Class A who earn between €352.01 and €424 in a week. Lower rate of 8.5% employer PRSI to apply to weekly earnings of up to €376.01 (up from €356.01).

Tax credits:

- home carer tax credit – an increase in the home carer tax credit from €810 to €1,000 and increase in the income threshold from €5,080 to €7,200; and

- Earned income credit – welcome introduction of an earned income credit of €550 for the self-employed and business owners/managers who are ineligible for a PAYE credit on their income.

Incentives:

- Home Renovation Incentive (HRI) extended until 31 December 2016; and

- Profits or gains from the occupation of woodlands removed from the high earners’ restriction.

Agri-food sector

General stock relief, stock relief for young trained farmers, stock relief for registered farm partnerships and the Stamp Duty exemption for young trained farmers extended to 31 December 2018. A new farm succession transfer partnership model to be introduced, subject to EU state aid approval.

Child benefit

Child benefit is to increase by €5 per month to €140 per child from January 2016.

State pension

€3 increase per week for pensioners and carers aged 66 and over.

Pensions:

- tax relief for pension contributions continues at the marginal rate of tax;

- pension levy – the 0.15% pension levy introduced for 2014/2015 will be abolished with effect from 31 December 2015.

Local Property Tax (LPT)

The Minister for Finance will be making a proposal to Government to postpone the revaluation date for the Local Property Tax from 2016 to 2019.

Banking Levy

It is proposed to extend the banking levy, which is currently due to expire in 2016, by five years to 2021, subject to a review taking place of the methodology used to calculate the levy.

Corporate tax

Knowledge Development Box (KDB)

Profits arising from certain patents and copyrighted software, which are the result of R&D carried out in Ireland, will be taxed at a rate of 6.25%. The KDB will be in line with the recent OECD guidelines and will be the first and only box of its kind in the world to meet the new standards of the OECD’s “modified nexus” approach.

International corporate tax – OECD

Base Erosion Profit Shifting (BEPS) The Government has published an update on Ireland’s international tax strategy and reaffirms its commitment to the OECD BEPS project. The 12.5% corporation tax rate on trading profits will not be changed as the OECD has confirmed that each country is free to set its corporation tax rate.

The Government intends to finalise the Multilateral Instrument (MLI) by the end of 2016 and deliver on a number of changes as proposed by the OECD as part of the BEPS project.

In order to enhance transparency in our tax system, Minister Noonan has implemented the Country by Country transfer pricing reporting regime as outlined in the BEPS project. This applies for accounting periods commencing on or after 1 January 2016.

Employment and Investment Incentive Scheme (EIIS)

The amount of finance that can be raised by a company under EIIS has increased from €2.5m to €5m annually. This will be subject to a lifetime maximum of €15m, up by €5m. The scheme will now be available to all SMEs irrespective of their geographical location. Finally, the scheme has been expanded by allowing investments in the extension, management and operation of existing nursing homes. These changes are effective from midnight tonight.

Film relief

There is to be an increase in the cap for eligible expenditure qualifying for film relief from €50m to €70m; this limit will be reviewed going forward.

Other measures

Corporation tax relief for start-up companies has been extended for a further three years. This is based on the number of employees and loss-making companies may carry forward unused relief.

The Start-Up Relief for Entrepreneurs (SURE) has been extended by including investments in the extension, management and operation of nursing homes.

The scheme of capital allowances for the construction of facilities used in the maintenance, repair, overhaul and dismantling of aircraft is being amended to comply with EU state aid rules. The scheme commences from 14 October 2015.

Indirect taxes

- VAT – no change in any of the existing VAT rates, including the 9% rate for tourism sector and farmer’s flat rate addition, which remains at 5.2%;

- Excise – the excise duty on 20 cigarettes is being increased by 50c (including VAT) with effect from midnight 13 October, with pro rata increases for other tobacco products. This will increase the price of most popular brands to €10.50. There are no changes in the rate of duty on petrol, diesel or alcohol;

- Commercial road tax on goods vehicles – the rates of motor tax and the number of tax classes will be significantly reduced from 1 January 2016.

- The current number of classes will be reduced from 20 to 5 with rate ranging from €92 – €900 (the current maximum is €5,195);

- Micro-breweries – micro-breweries qualify for a special relief from alcohol products tax where output does not exceed 30,000 hectolitres per annum. As a cash flow measure, this relief will be available upfront as well as by means of a rebate;

- Electronic payments – to encourage the use of electronic payments by debit cards and discourage the withdrawal of cash from ATMs, the €2.5/€5 Stamp Duty on ATM/debit cards will be replaced with a 12c charge per ATM transaction (subject to overall cap at the existing annual stamp duty level). There will be no charge for debit card transactions. The transaction limit on contactless payment cards is being raised from €15 to €30 from 31 October 2015; and

- VAT and charities – the Department of Finance is examining proposals set out in the VAT on Charities Working Group Report, published in October 2015, to reduce the VAT burden on charities. This may take the form of a refund process.

Capital taxes

- Capital Acquisitions Tax (CAT) – the Group A tax free threshold has been increased from €225,000 to €280,000 with effect from 14 October 2015. This threshold generally applies to gifts and inheritances from parents to their children. No change to other group thresholds. No change to the rate of CAT, which is currently 33%; and

- Capital Gains Tax (CGT) – entrepreneurs’ relief – from 1 January 2016, a CGT rate of 20% (rather than the standard rate of 33%) shall apply to the net chargeable gain arising on the disposal by individuals of assets comprising the whole or a discrete part of a trade or business. This shall be subject to a lifetime limit of €1m. Thus, based on current CGT rates, the maximum tax benefit is €130,000.

See the full facts with our in-dept budget summary for 2016 report

Please click here to download the full budget summary for 2016